Keir Starmer’s 2022 Labour Party conference speech sketched out his strategy to occupy the political ground vacated by Trussonomics.

Labour would put working people interests over those of the rich, be the party of opportunity, of aspiration, of fairness, as well as of sound public finances and of economic competence.

Kwasi Kwarteng’s September mini-budget comprising £45bn of tax cuts – the biggest since 1972- with its immediate economically and politically disastrous aftermath provided a helpful backdrop to resonate his message to define the ideological blue water between Labour and Conservative, largely hidden during the May and Johnson administrations.

Trussonomics is essentially Reaganomics (relying on tax cuts on the rich to spur growth) mixed with Modern Monetary Theory – it is basically OK for governments that issue and borrow in their own currency to resort to money-printed deficit funding until an unsustainable inflation inflection point is reached.

In short, it is the Conservative free market equivalent of Corbynism, save that: the rising tax unfunded deficit will be the result of taxes being cut rather than of spending increased; John McDonnell was more wedded to fiscal sustainability and would have unlikely to have introduced discretionary spending unfunded increases to take the deficit to 7.5% of GDP, and if he had, would have prepared the ground better with the financial markets in a more pragmatic fashion; the aim is to achieve a 2.5% headline growth rate just before a 2024 election – regardless of its sustainability and the ability to fund future health and other core social welfare activity – is more political cynical and single-minded in its pursuit of perceived party over national interest.

It is unlikely that will come to pass even on its own terms. Evidence is lacking that tax cuts concentrated on the top five per cent will lift growth – Reagan’s tax cuts in the 80’s led to a ballooning public deficit that had to be closed later. It suggests instead that increased inequality retards rather than helps sustainable growth.

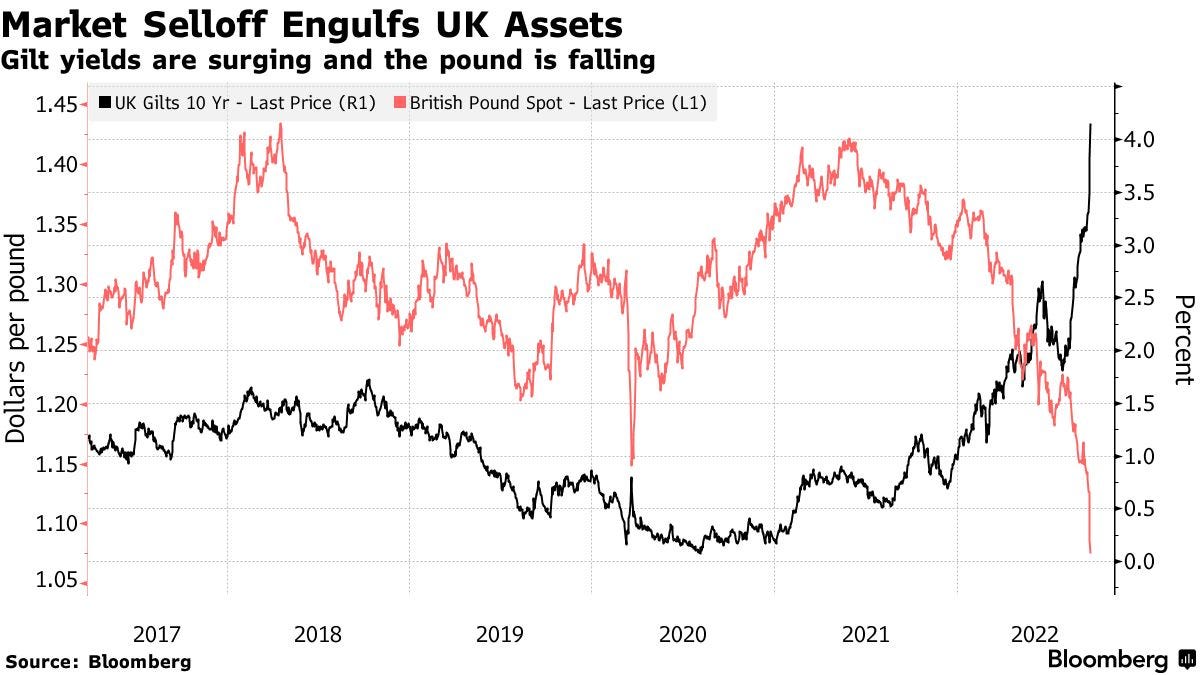

Embarking on unfunded borrowing to pay for tax cuts at a time when the public deficit is near to a record high, the balance of payments current deficit is widening, inflation is at a 30 year high, and when sterling was already weak, was asking for trouble. It soon came as the following chart showed.

{kind=link}

Fiscal and monetary policy are now actively working against together to such an extreme that the Bank of England had to resort within days to a £65bn purchase of long-dated government bonds (gilts) to stop a calamitous sell off by pension funds facing margin calls due to bond prices collapsing in response to the sudden rise in gilt yields.

Most commentators expect mortgages rates to approach 6% by 2023. Combined with sterling at near parity with the dollar (which increases import costs) living standards on the vast majority will be squeezed that much tighter and first-time buyers thwarted as mortgage costs become unaffordable. Outcomes that will heavily weigh down on growth making the tax cuts self-defeating in the process.

The political optics of reducing taxes on the already rich at a time when most working households are struggling to juggle their budgets with many without savings facing real hardship was also dire.

Kwarteng thus gave Starmer practically an open goal to shoot at. Shrouding his speech with his family backstory, parental struggle in a pebble-dashed semi, their hard work and aspiration accorded with the approach suggested in Starmer’s Story Must Be Labour’s Story.

The headline flagship of his speech was 100% clean energy by 2030. Public-private partnerships spearheaded by a new Great British Energy state undertaking established within the first year of a new Labour government would unlock investment in domestic renewable energy sources to create a “million new jobs training for plumbers, engineers, software designers, technicians, builders” as well as insulate 19 million homes.

Complementing the £8bn National Wealth Fund that the shadow chancellor, Rachel Reeves, had announced the previous day, all this was rather suggestive of a green updating of Harold Wilson’s White Heat of Technological Revolution pre-1964 election banner, creating British jobs on the back of British innovation and investment.

Growth would also be bolstered by targeted capital allowances and borrowing to invest for long-term economic benefit within a wider fiscal framework where the current budget would be balanced: a resurrection of Gordon Brown’s golden rule. Fiscal rules would require debt as a proportion of GDP to reduce, with all policy commitments fully costed and funded, guided by (a previously announced) Office for Value for Money.

To support the customary Labour commitment to safeguard the NHS, more nurses, midwives, and doctors would be trained, funded from the proceeds of a reimposed 45% higher rate; in effect, a sleight of hand, insofar that reversing a cut simply restores to previous position: by the same logic reinstating the national insurance increases and Health and Social Care Levy would create the opportunity for £16bn of spending on new commitments.

70% home ownership would be sought by a policy framework favouring first time buyers (FTB) rather than Buy-to-Let investors and second home purchasers. Foreign purchasers would be charged a higher rate of transaction stamp duty, while a Mortgage Guarantee Scheme would aim to reduce FTB deposit requirements.

Such a commitment without some systemic reform of the current housing system based on private business models dependent on rising house prices, appears to risk becoming a false target akin to the Conservative 300,000 homes one, diverting attention from the substance of strategic policy change although mention was made to “reform planning so speculators can’t stop communities getting shovels in the ground”, which, however, is a slogan rather than a policy.

There were some other specific taxation pledges, namely retaining the reduced 19% basic rate and not reversing the national insurance increase – and relatively unremarked on – abolishing business rates, replaced with an alternative system (undefined) that would provide for early payment of revaluation discounts.

In that light, no indication was given how Boris Johnson’s existing September 2021 social care package – let alone an improved fairer one – would be financed nor was note made of the impact of Kwarteng’s tax cuts on its current progress.

Taxes on workers and employers have deadweight effects on employment, wages, productivity and growth, but given the public finances will be in mess if and when Labour forms a new government, such commitments beg questions as how spending on rising health care and social care needs in an aging society, on further education conducive to growth, on investment in affordable housing and bringing private sector housing up to Decent Homes Standard, is to made compatible with Labour’s proposed fiscal framework.

To square that circle is a long odds gamble on growth and lower interest rates coming to the rescue of the real crisis of the fiscal state: the mismatch between the public expenditure requirements of the UK and the political and electoral willingness for them to be met through forms of taxation that are efficient, sufficient, and transparent.

Honest and deep debate on public funding requirements matched to sources is accordingly avoided, invariably subverted instead to short-term political presentational purposes. The impoverishment of public services and an almost default governmental resort to hidden stealth or inefficient forms of taxation is the inevitable end-result.

In that light, it was disappointing that Starmer’s speech appeared to accept the Conservative take on the that taxes need to reduce, resorting to a New Labour-type tactical triangulation response, such as the linkage of increased spending on doctors and nurses with a reimposed 45% tax rate.

He could have focused instead on the trade-off between investing for growth and tax cuts, highlighting the impact of frozen tax allowances as a prime example of taxation by stealth on the hard-working majority, linking it to the need for system reform across the health and social care, housing and education sectors.

Strategy and tactics need to be rebalanced over the coming year.